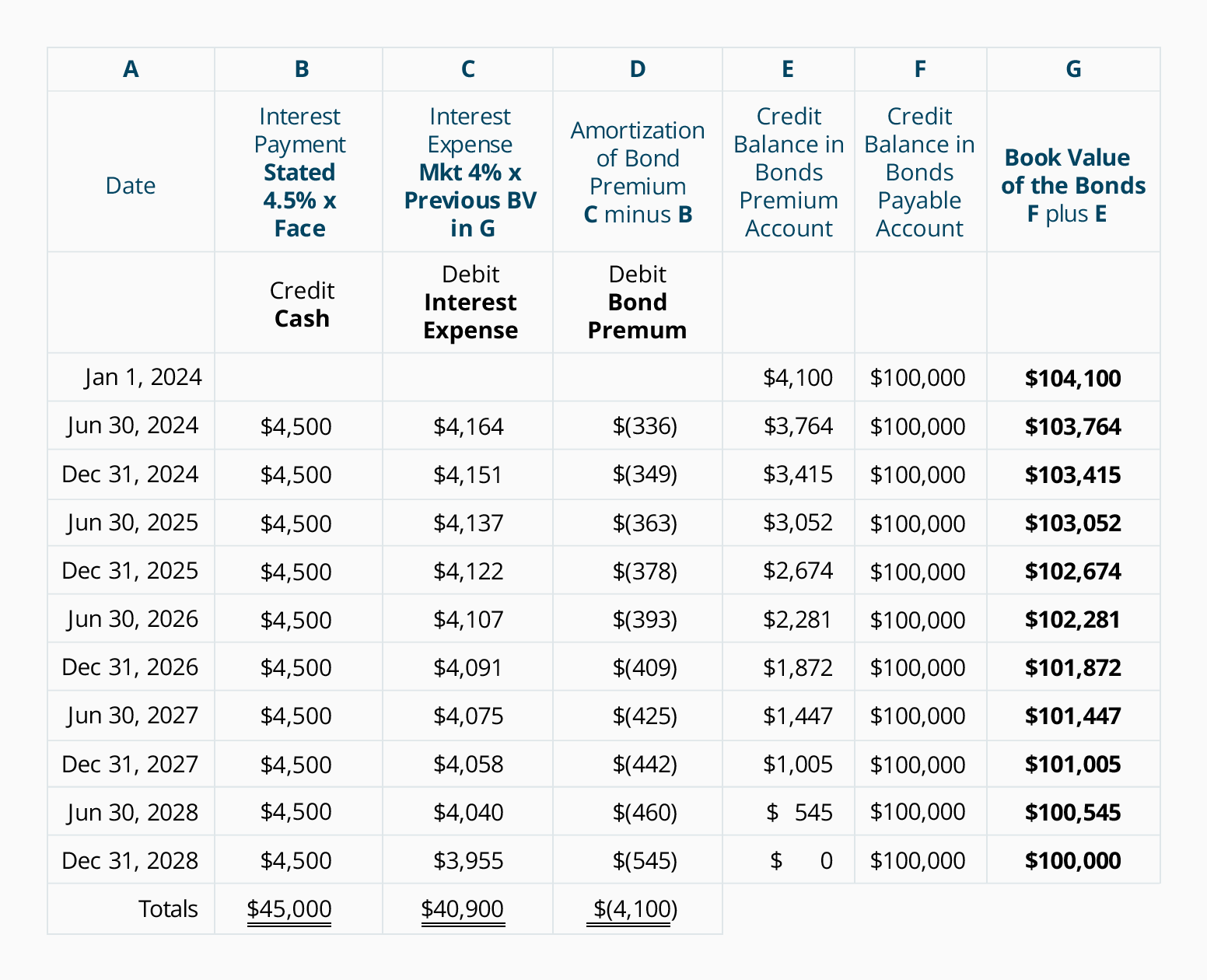

At the end of the third year premium bonds payable will be zero and the carrying amount of bonds payable will be 100000. This is classified as a liability and is amortized to interest expense over the remaining life of the bonds.

Accounting For Bonds Payable Principlesofaccounting Com

Home Accounting Dictionary What is a Premium on Bonds Payable.

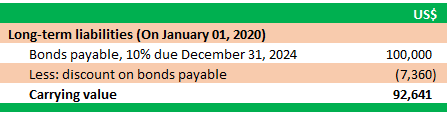

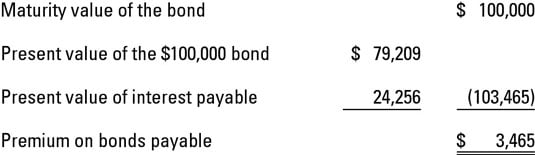

Premium bonds payable. This is classified as a liability on the books of the issuer and is amortized to interest expense over the remaining life of the bonds. As the balance in the premium on bonds payable account declines over time this means that the net amount of the bonds payable account and premium on bonds payable account presented in the balance sheet will gradually decrease until it is 10000000 as of the date when the bonds are to be repaid to investors. Premium on bonds payable is the excess amount by which bonds are issued over their face value.

Is discount on bonds payable. What is a Premium on Bonds Payable. Premium on bonds payable or bond premium occurs when bonds payable are issued for an amount greater than their face or maturity amount.

Instead the interest rate funds a monthly prize draw for tax-free prizes. Can I move money from another NSI account to Premium Bonds. Premium on bonds payable is the excess amount by which bonds are issued over their face value.

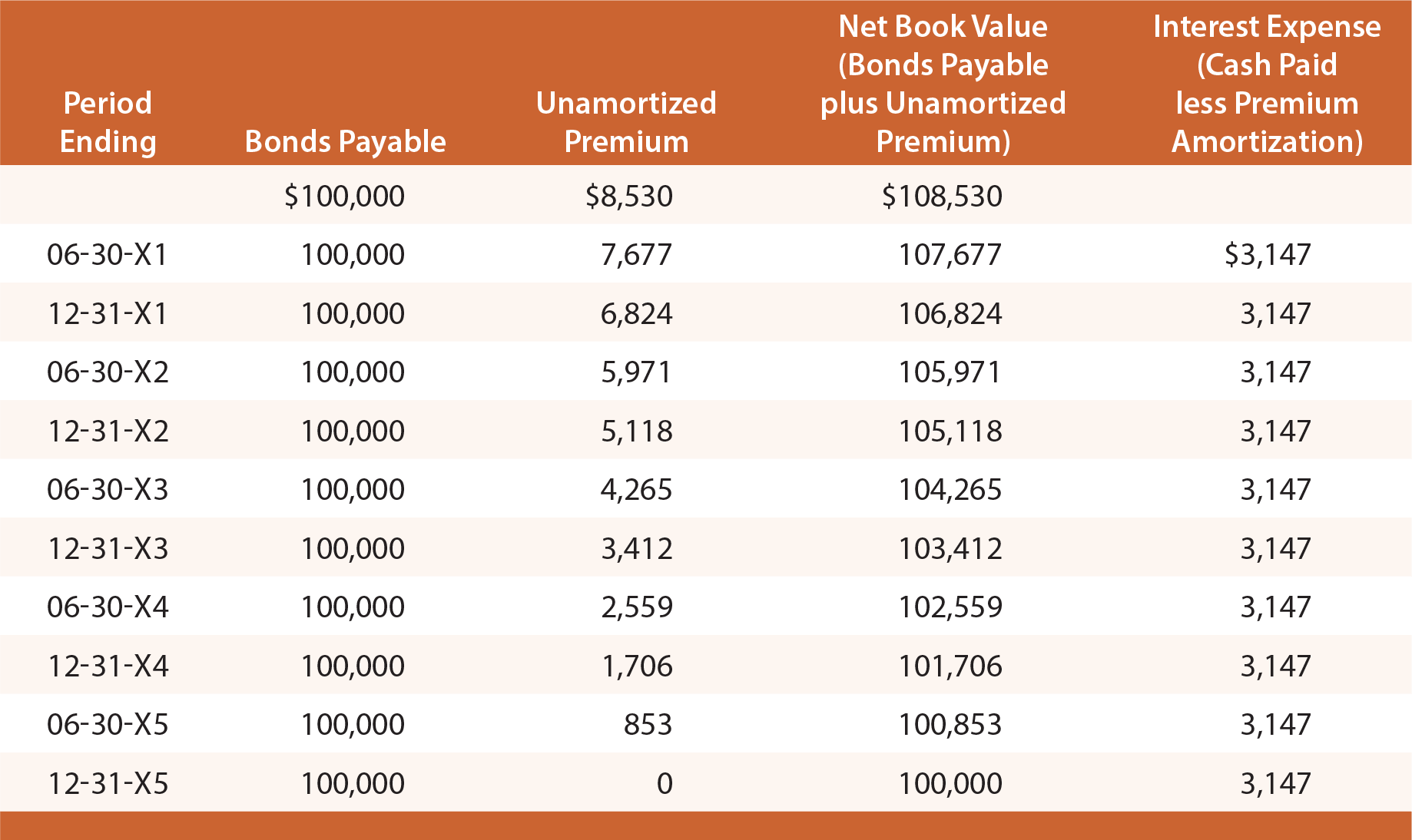

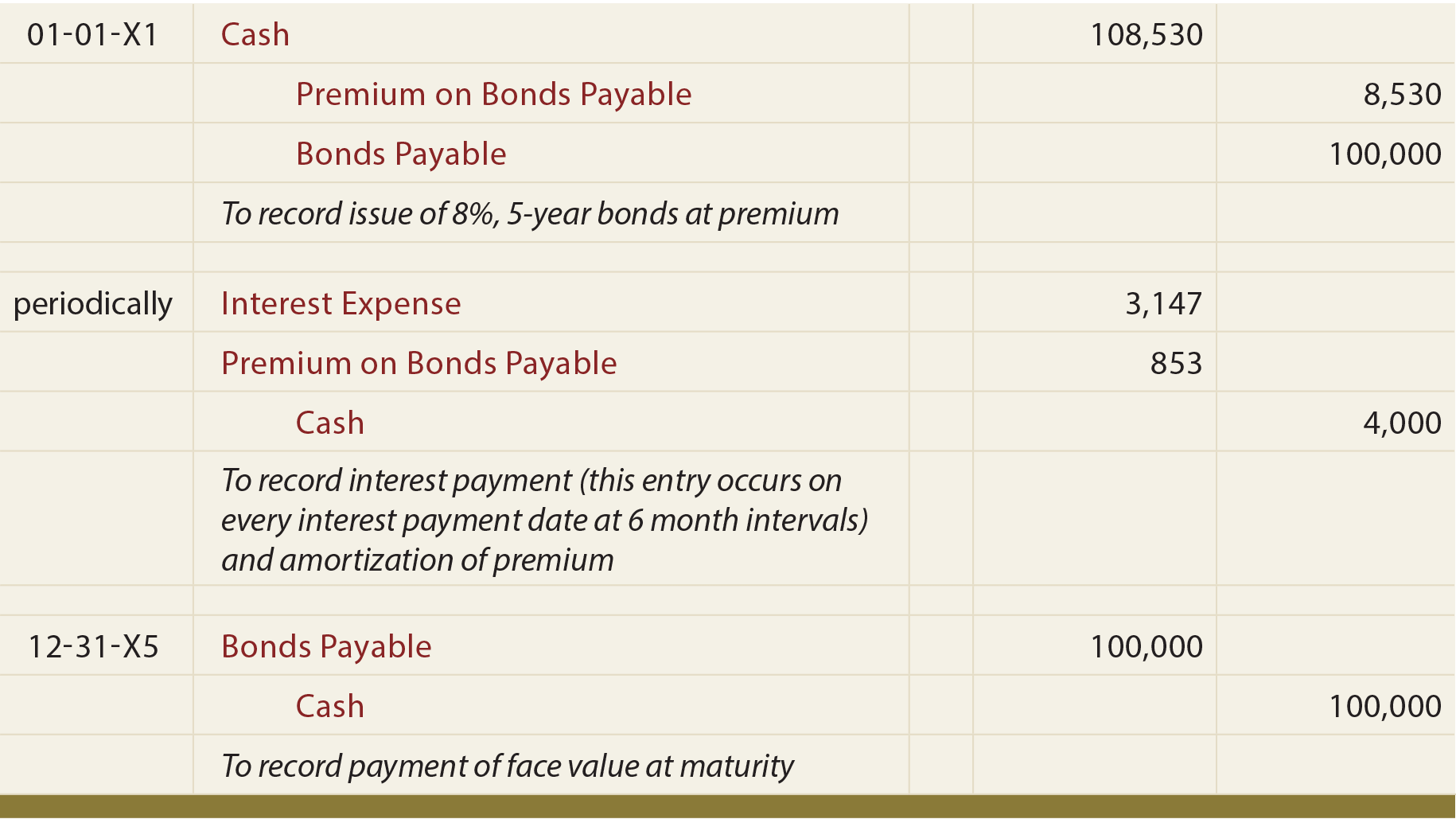

A premium on a bonds issue arises when the interest rate being paid on the bond referred to as the coupon rate is higher than the equivalent market interest rate at the moment. Study the following illustration and observe that the Premium on Bonds Payable is established at 8530 then reduced by 853 every interest date bringing the final balance to zero at maturity. The amount received for the bond excluding accrued interest that is in excess of the bonds face amount is known as the premium on bonds payable bond premium or premium.

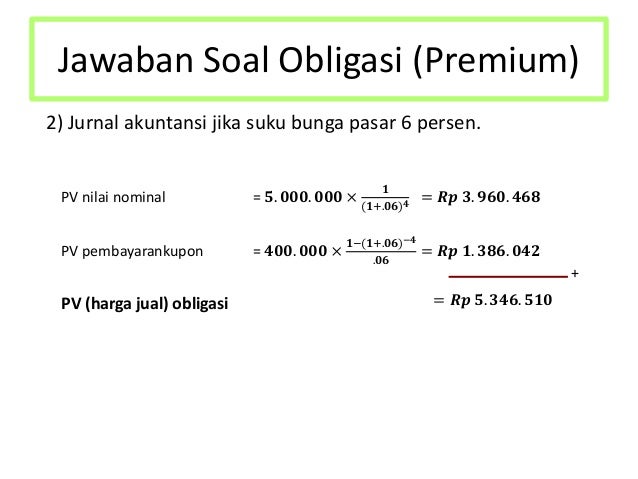

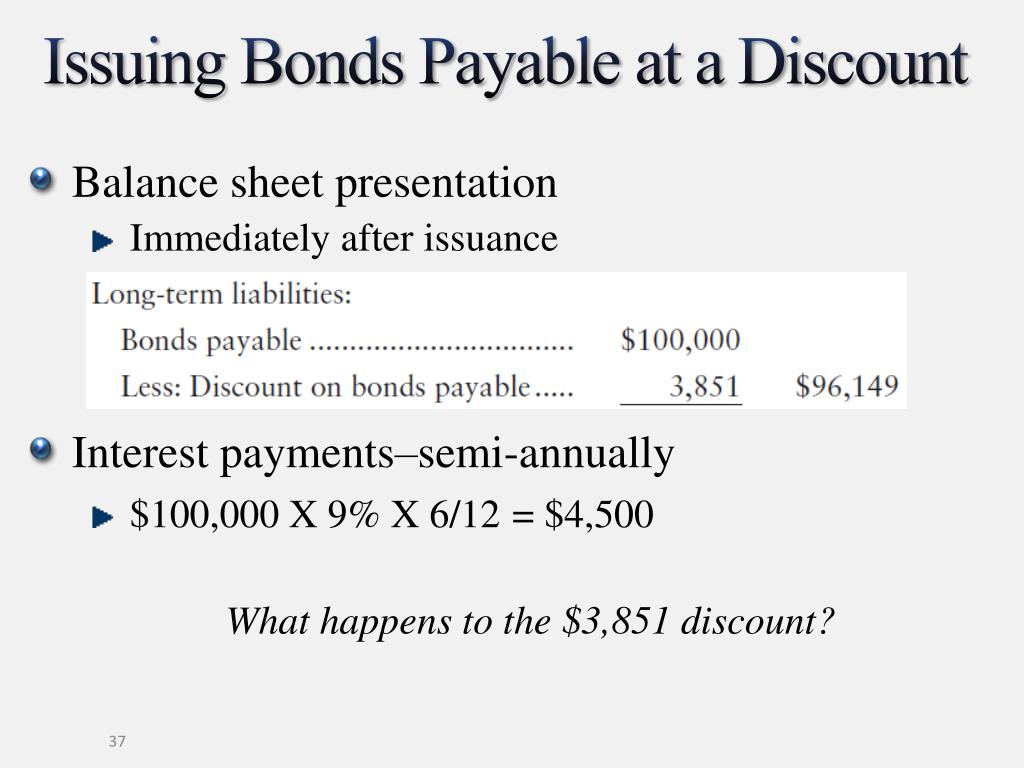

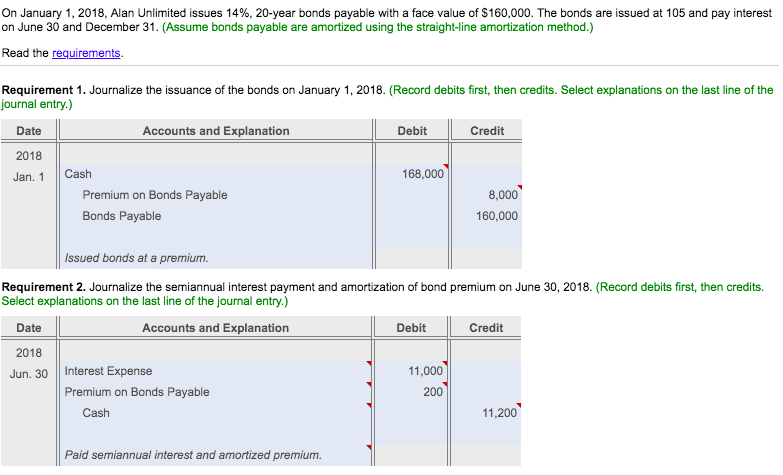

Like the discount situation we looked at in our other article this raises three issues we need to look at. Like the discount situation we looked at in our other article this raises three issues we need to look at. Bond Interest and Principal Payments.

So on the balance sheet carry value is 102577 which is the present value of cash flow. Bonds Payable Issued at a premium. Discount on bonds payable 6074.

At every coupon payment interest expense will be incurred on the bond. Also with the added yield the bond trades at a premium in the secondary market for a price of 1100 per bond. What is premium on bonds payable.

Premium on bonds payable 17730. On issuance a premium bond will create a premium on bonds payable balance. Remember that inflation can reduce the true value of your money over time.

The balance of premium on bonds payable will be included in financial liability-bonds. Interest expense 5887. Bonds payable are a form of long term debt usually issued by corporations hospitals and governments.

With Premium Bonds there is no interest earned. Premium on bonds payable is the excess amount by which bonds are issued over their face value. For example a bond with a stated interest rate of 8 is sold.

The difference between these two numbers is considered the bond premium. A premium on bond occurs when the bonds par value is lower than the issue price or carrying value. The net effect of this amortization is to reduce the amount of interest expense associated with the bonds.

What is a Premium on Bonds Payable. Cash 10000 Discount journal entries for 2008. Premium on bonds payale 4113.

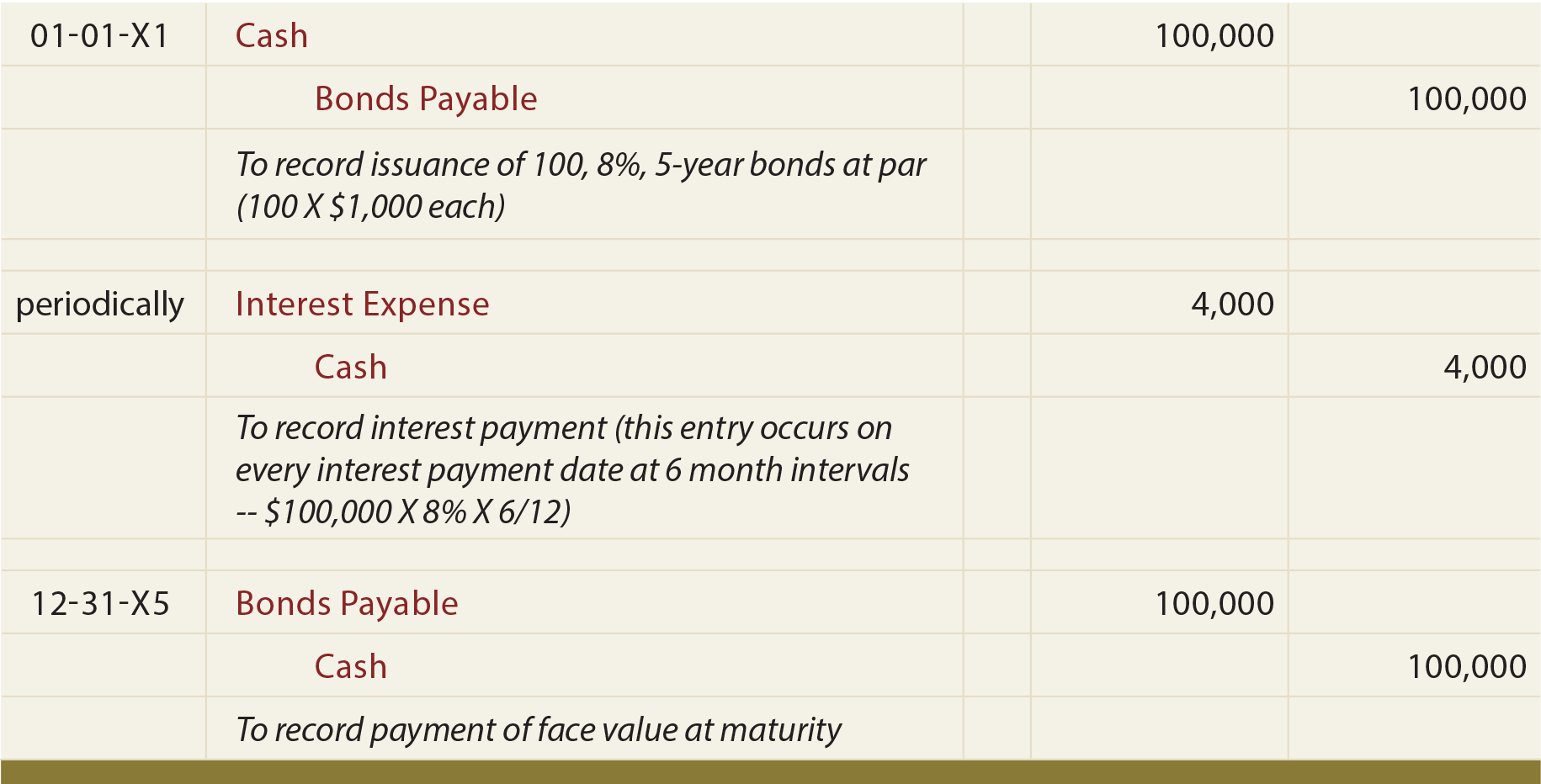

A premium on a bonds issue arises when the interest rate being paid on the bond referred to as a the coupon rate is higher than the equivalent market interest rate at the moment. The issuer of bonds makes a formal promiseagreement to pay interest usually every six months semiannually and to pay the principal or maturity amount at a specified date some years in the future. This is classified as a liability and is amortized to interest expense over the remaining life of the bonds.

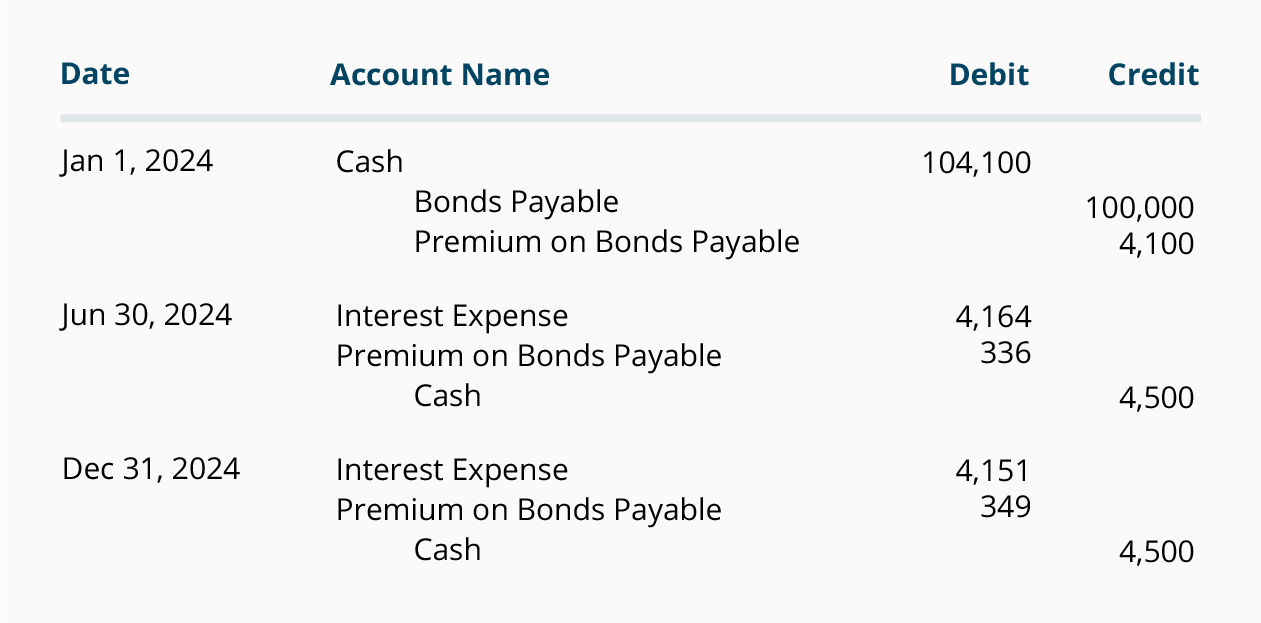

Premium on bonds payable is the excess amount by which bonds are issued over their face value. This is caused by the bonds having a stated interest rate that is higher than the market interest rate for similar bonds. Bonds Payable Issued at Premium Journal Entry The bonds payable would be issued at a premium value of 108111 and the journal entry to record this would be as follows.

In return bondholders would be paid 5 per year for their investment. This is classified as a liability on the books of the issuer and is amortized to interest expense over the remaining life of the bonds. To illustrate the premium on bonds payable lets assume that in early December 2019 a corporation has prepared a 100000 bond with a stated interest rate of 9 per annum 9 per year.

In this case investors are willing to pay extra for the bond which creates a premium. If a bond is issued at a premium or at a discount the amount will be amortized over the years through to its maturity.

Pengantar Akuntansi 2 Bonds Payable

What Were The Calculations That Were Done To Get Chegg Com

Bonds Payable

How To Record Bonds Issued At A Premium Dummies

Premium On Bonds Payable Example Youtube

Ppt Long Term Liabilities Bonds Payable And Classification Of Liabilities On The Balance Sheet Powerpoint Presentation Id 1672705

Journal Entry For Bonds Accounting Hub

Accounting For Bonds Payable Principlesofaccounting Com

Bonds Payable In Accounting Double Entry Bookkeeping

Accounting For Bonds Payable Principlesofaccounting Com

Ppt Long Term Liabilities Bonds Payable And Classification Of Liabilities On The Balance Sheet Powerpoint Presentation Id 1672705

Bonds Payable

Amortizing Bond Premium Using The Effective Interest Rate Method Accountingcoach

Amortizing Bond Premium Using The Effective Interest Rate Method Accountingcoach

Accounting For Bonds Payable Principlesofaccounting Com

Longterm Liabilities Bonds Payable And Classification Of Liabilities

C 14 Indo Intermediate 2

What Were The Calculations That Were Done To Get Chegg Com

Ppt Long Term Liabilities Bonds Payable And Classification Of Liabilities On The Balance Sheet Powerpoint Presentation Id 1672705